A Plan to Get Ahead of Your Debt

Do you have a plan to get ahead of your debt, even as households currently face price increases for everyday essentials?

Rising prices are putting pressure on family budgets – especially items like groceries and gas. A recent NFCC and Wells Fargo poll showed that 26% of Americans are more worried about meeting basic household expenses compared to 12 months ago.

Need a Little More Support?

GreenPath’s Debt Management Plan consolidates your debt into a single payment. Each payday, you automatically deposit money into your GreenPath account, and we use that money to pay on your behalf. We may be able to arrange lower interest rates and monthly payments with your creditors, so you can pay off debt faster and save money.

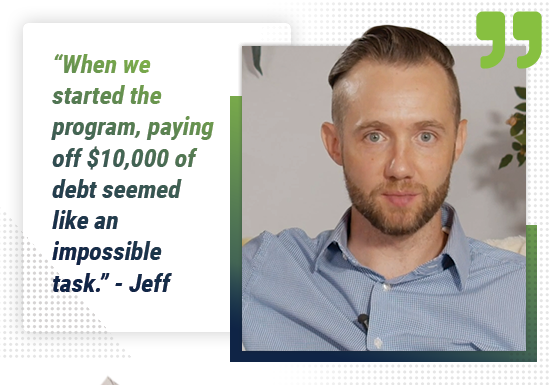

Get Out of Debt Faster with A Debt Management Plan

GreenPath’s Debt Management Plan consolidates your debt into a single payment. Talk to a counselor to see if this is the right move for you. The call is 100% free, no pressure.

To handle the rising costs of everyday expenses, many people lean on their consumer credit cards. Recent data shows that household debt balances for auto loans, credit cards and student loans rose to $4.25 trillion (Federal Reserve Bank of New York).

These trends mean that managing debt is becoming even more important than ever.

This is where a trusted, national nonprofit like GreenPath comes in. To reduce stress, it’s helpful to get advice and an action plan to get you on track to pay off debt and build a healthy financial life.

Our trusted debt management services help you pay debt off faster, save money on fees and interest, and make progress toward financial fitness.

Tips to Get Ahead of Your Debt

While connecting with GreenPath is a great option, there are additional tips you can take as a first step to get ahead of your debt.

A Trusted National Nonprofit

GreenPath Financial Wellness is a trusted national nonprofit with more than 60-years of helping people build financial health. Start a conversation with a counselor.

- Take care of essentials first — housing, medicine, food, utilities, childcare and transportation.

- Think of a budget – or spending plan – as a roadmap. Assess your monthly income against current expenses. Has your income increased, decreased or remained steady? Utilize a budgeting worksheet to track monthly income (what’s coming in) and all your expenses (what’s going out). Figure out what is your new baseline if hours have been cut or there’s a loss of income. Also, take a hard look at your spending. Are you spending more than what you earn? How have your expenses changed, given the rising cost for everyday items? Limit credit card use and curb discretionary spending such as eating out (plan your meals), cable/streaming services or subscriptions temporarily (or negotiate these costs).

- Leverage available federal, state and local assistance. Most states are slowly receiving American Rescue Plan Act (ARPA) funds from the Homeowner Assistance Fund (HAF) that will help households who have fallen behind on their mortgages and other housing-related expenses due to COVID-19. Check your local housing authority for more information.

- Contact your lenders, creditors and landlords sooner than later to have an honest conversation about available hardship options. When you team with GreenPath, we can streamline this important task and connect with your creditors on your behalf.

- Build an emergency fund — not a ‘nice to have’ but a necessity, so that you don’t go into debt to cover an emergency expense. If your washing machine will need to be replaced in the coming months, try to set aside cash now. Put savings on autopilot with each paycheck (set it and forget it). Even a small amount will add up over time.

- Make room in the budget now/early to resume paused payments. Contact your loan servicer to update contact information, see if you’re eligible for an income-driven repayment plan or (public service) loan forgiveness. See if your employers can make contributions towards eligible education expenses.

- Choose a debt payoff strategy that works for your situation. Consider a Debt Management Plan which helps you pay off unsecured debt in 3 to 5 years. GreenPath works with your creditors to bring your accounts current, lower interest rates, and eliminate fees. More of your payment goes toward reducing your account balance and you save money on interest.

Let’s Get Ahead of Your Debt Together

Even in the face of rising prices and other financial uncertainties, our clients have told us that it is easier to make healthy financial choices when they have strong options at their fingertips.

As a trusted national nonprofit serving people for more than 60 years, our clients get ahead of debt with a debt management plan program designed to improve and promote financial wellness.

Talk to GreenPath Today

With more than 60-years of helping people build financial health, our financial counselors are here to help.