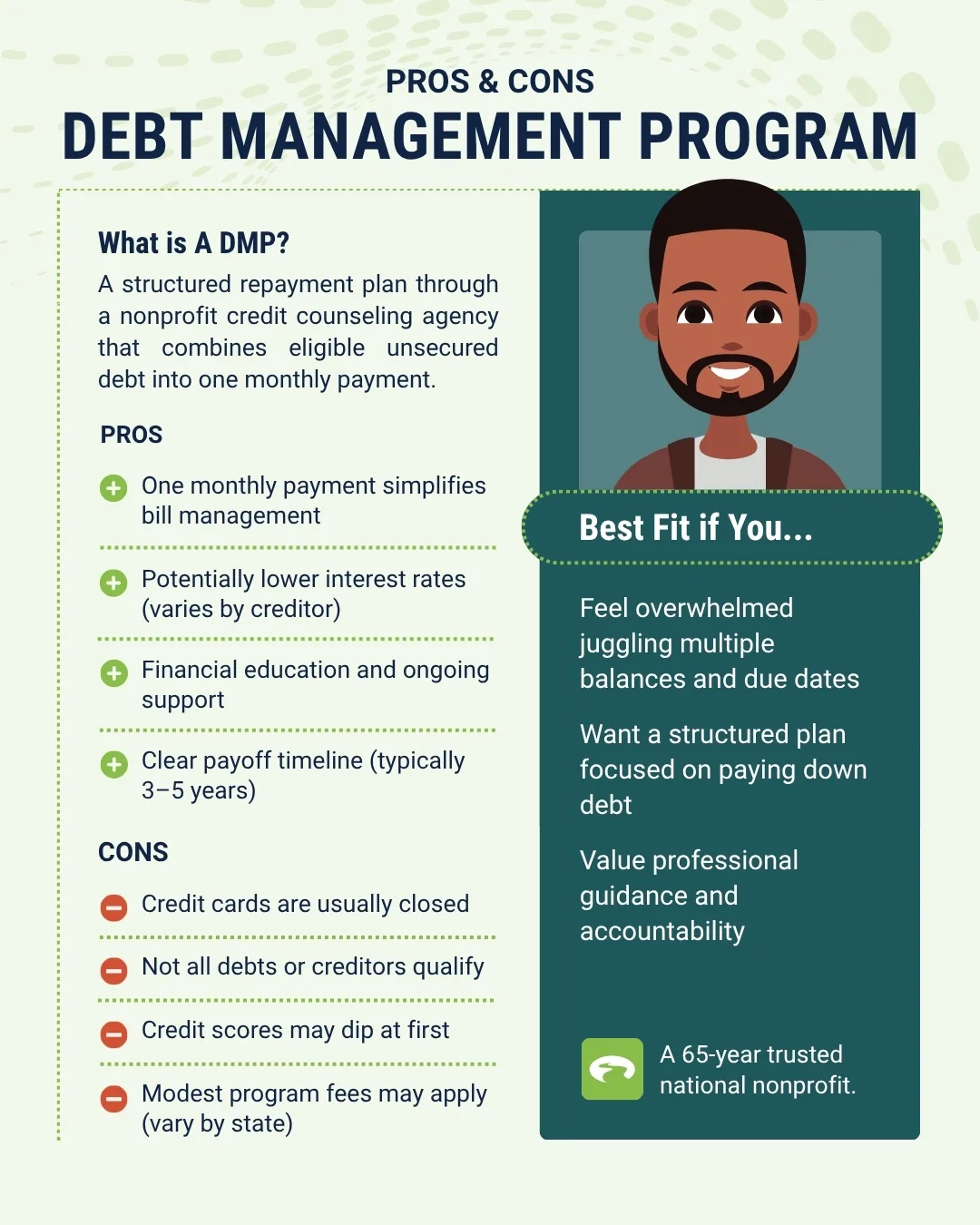

A debt management program (DMP)debt management program (DMP) is a structured way to repay eligible unsecured debt in full through one monthly payment, often with reduced interest rates.

DMPs can simplify repayment and ease stress, but tradeoffs include closed cards, possible short-term credit impacts, and the reality that some debts or creditors may not be eligible.

Whether a DMP is right for you depends on your debt type, ability to make steady payments, and comfort with short-term credit score changes.

High-interest debt is incredibly common today.

And while knowing you’re not alone can be comforting, dealing with overwhelming debt is still stressful and confusingstressful and confusing. For many people, it doesn’t happen because of poor choices. It builds up gradually through everyday expenses, rising rates, and life curveballs that are hard to plan for. You need real solutions—and clear information—to regain control.

One option worth understanding is a debt management program (DMP), which provides a structured repayment plan through a nonprofit credit counseling agency.

DMPs can be helpful in the right situations, but no two financial pictures look the same. Our goal is to help you understand how they work—so you can decide what makes sense for you.

What Is a Debt Management Program (DMP)?

U.S. household debt reached an all-time high of nearly $18.8 trillion in 2025, according to the Federal Reserve Bank of New York.

Being in debt doesn’t mean you’re stuck forever, but how you tackle it matters.

A Debt Management Program (DMP) is a structured repayment program offered by nonprofit credit counseling agencies. If a DMP is right for your situation, the agency helps you create a personalized payoff plan based on what you can realistically afford.

Rather than taking out a new loan, a DMP simplifies repayment by combining eligible unsecured debts into one monthly payment, which the agency distributes to participating creditors. Most plans aim to repay enrolled debts in three to five years.

Think of the DMP as the process—and the debt management program as the customized repayment roadmap that comes out of it.

Important: DMPs Are for Unsecured Debt

Debt management programs typically apply only to unsecured debts, such as:

- Credit cards

- Personal loans

- Some medical debt (depending on the creditor)

Debts backed by collateral—like mortgages, auto loans, and most student loans—generally cannot be included in a DMP.

Unpaid unsecured debt can lead to:

- Credit score damage

- Fees and higher interest rates

- Collections activity or legal action

- Increased stress

Debt Management Program Pros

One Monthly Payment

A DMP simplifies repayment into one consistent monthly payment, which can make managing multiple bills more manageable. That simplicity can reduce the mental load of juggling due dates and help you stay consistent, especially when money feels tight.

Lower Interest Rates (When Creditors Participate)

Participating creditors may agree to reduce interest rates, which can help more of your payment go toward principal. When rates are reduced, many people feel they finally gain traction—because more of each payment can go toward what they owe, not just interest.

Possible Fee Waivers

Some participating creditors may waive certain fees—such as late or overlimit fees—after accepting the plan. Fewer fees can make your payoff plan feel more predictable and help keep your payment focused on progress rather than penalties.

Fewer Collection Contacts

Once creditors accept the program and payments are made on time, many consumers experience fewer collection calls or notices. That can create breathing room so you can focus on following your plan instead of reacting to constant outreach.

Ongoing Counseling and Support

You’ll receive check-ins and accountability throughout the program. You also get a clearer view of your options (and a realistic plan built around your budgetbuilt around your budget) so you’re not guessing your way forward.

Building Credit Health

A DMP itself doesn’t raise your credit score. However, consistent on time payments and shrinking balances can help improve credit over time. Scores may dip early due to account closures. The bigger win is building steadier repayment habits—on time payments and lower balances are the kinds of factors scoring models reward over time.

A Defined Timeline

Most plans are designed to repay enrolled debt within three to five years, giving you a clear endpoint. Having a target finish line can make the process feel more doable—and help you trade uncertainty for a plan you can measure month by month.

Debt Management Program Cons

Credit Cards Are Often Closed

Most programs require closing enrolled credit card accounts, which can temporarily affect credit scores and limit access to credit. Depending on your situation, you may be allowed to keep one credit card account open for emergencies.

Not All Creditors Participate

Some debts may remain outside the program and require separate payments. That’s why it helps to review which accounts are eligible upfront—so you can plan for any “outside the program” payments alongside the DMP payment.

It Takes Time

DMPs are designed for steady repayment, not immediate relief. If you’re seeking a faster solution (for example, because of an urgent hardship), counseling can help you compare other options and understand the risks involved before you move forward.

Some Debts Aren’t Eligible

Secured debts and most student loans aren’t included. If most of your debt is secured or student loan related, a DMP may have limited impact; another reason a full review during counseling is helpful.

Credit Score Impact Can Be Mixed

Account closures may cause an initial dip, but consistent payments can help rebuild credit over time. Your starting credit profile matters—someone already behind on payments may see different credit movement than someone who began with stronger credit.

Program Fees

Most plans are designed to repay enrolled debt within three to five years, giving you a clear endpoint. Having a target finish line can make the process feel more doable—and help you trade uncertainty for a plan you can measure month by month.

A Smart Next Step: Get Clarity Before You Decide

If you’re unsure whether a debt management program is right for you, a free financial counseling sessionfree financial counseling session can help you make that decision with confidence. During counseling, you’ll review your full financial picture—your debts, interest rates, budget, and available options—and learn whether a DMP fits your situation or if another path makes more sense. There’s no obligation to enroll, just expert guidance to help you understand your choices and decide what’s realistic and sustainable for you.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.