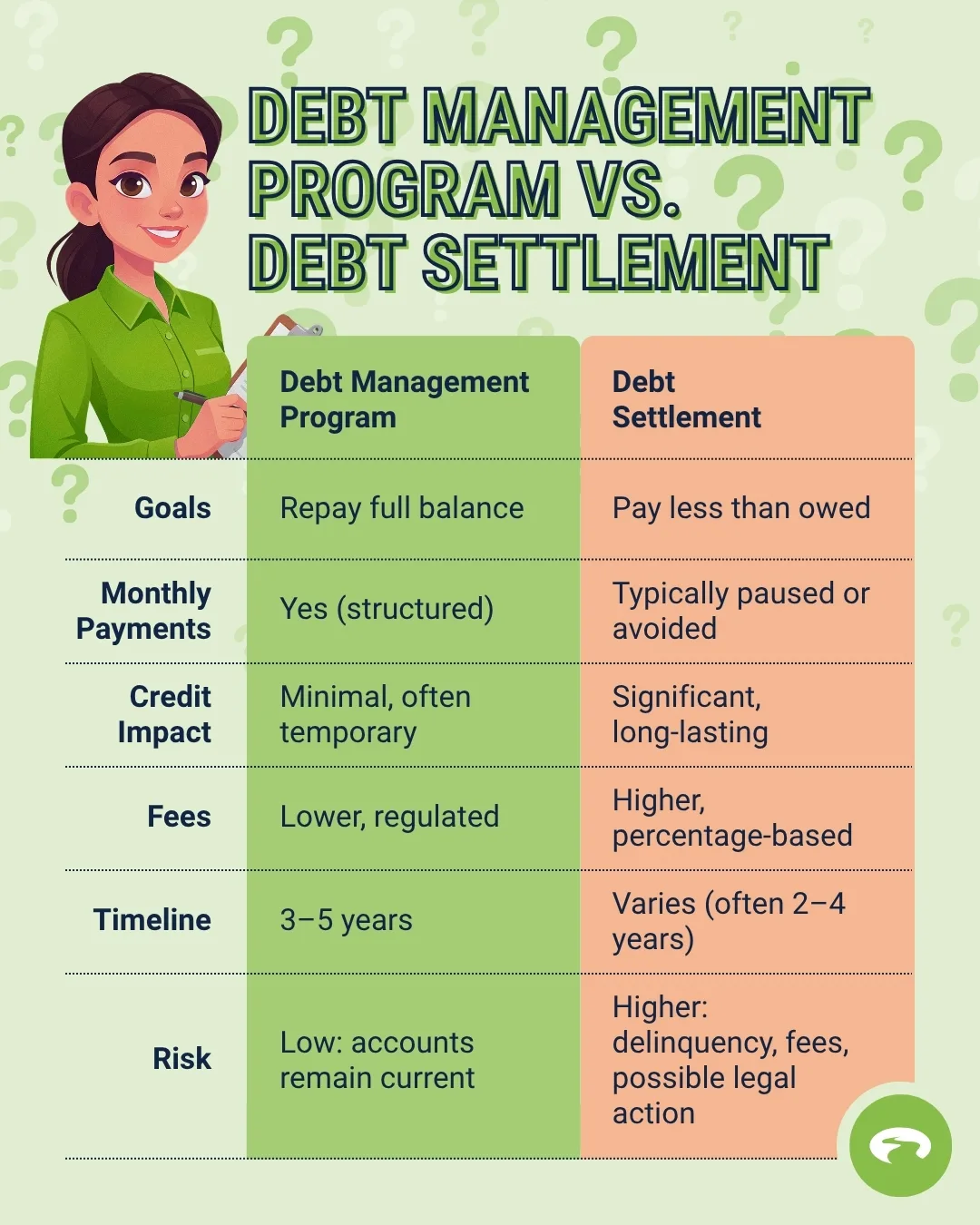

A debt management program helps you repay your full balance over time, often with reduced interest rates and one simplified monthly payment.

Debt settlement aims to reduce what you owe but can significantly impact your credit and comes with higher risk and uncertainty.

If you want structured, nonprofit support with less long-term credit damage, GreenPath can help you explore whether a debt management programdebt management program fits your situation.

Debt Settlement vs. Debt Management: The Short Answer

A debt management program helps you repay your full debt under better terms, while debt settlement involves negotiating to pay less than you owe—typically with greater risk, fees, and credit impact.

Why Understanding Your Debt Relief Options Matters

If you’re feeling overwhelmed by debt, you’re not alone. And you’re not without options. But here’s the problem: many debt relief solutions sound similar on the surface, while working very differently behind the scenes.

Two of the most common approaches—debt settlement and a debt management program—can both help you get out of debt. But choosing the wrong one for your situation can cost you time, money, and long-term financial stability.

What is a Debt Management Program?

A debt management program (DMP)debt management program (DMP) is a structured repayment plan typically offered through a nonprofit credit counseling agency. The goal is to help you pay off your debt in full, but under more manageable terms.

How a debt management program works

- You meet with a certified credit counselor to review your finances

- The agency works directly with creditors to potentially arrange lower interest rates and waive certain fees

- You make one combined monthly payment to the agency

- The agency distributes payments to your creditors

Most debt management programs are designed to be completed in three to five years, depending on your balance and payment capacity.

A debt management program is often a good fit if you’re still able to make consistent payments but need structure and relief.

Why people choose a DMP:

- Lower interest rates can reduce the total cost of repayment

- One predictable monthly payment simplifies budgeting

- A clear 3–5 year timeline helps you stay on track

- Debts are repaid in full, supporting long-term credit health

Important considerations:

- A DMP is a long-term commitment, not a quick fix

- You may need to close or stop using enrolled credit cards

- Modest setup and monthly fees typically apply

- Missing multiple payments could result in removal from the program

What is Debt Settlement?

Debt settlement is a more aggressive debt relief option that focuses on reducing the total amount you owe rather than repaying it in full.

How debt settlement works

- You (or a company) negotiate with creditors to accept less than the full balance

- Many strategies involve pausing payments to creditors

- Instead, you deposit money into a dedicated account

- Once enough funds are saved, a lump-sum offer is made

In some cases, creditors may agree to accept less than the full balance, but results vary widely and are never guaranteed. Because debt settlement often involves stopping payments and depends on creditors’ willingness to negotiate, the process is less predictable and typically results in significant credit damage.

In addition, balances may grow during the process due to fees and accrued interest, increasing both financial and emotional stress.

Risks and downsides of debt settlement

This is where debt settlement requires careful considerationrequires careful consideration.

Key risks:

- Significant credit score damage due to missed payments

- Late fees and interest may continue to accumulate

- Creditors are not obligated to accept settlement offers

- Fees are often high (typically a percentage of enrolled debt)

- Forgiven debt may be considered taxable income depending on your situation

Reputable debt settlement companies generally only charge fees after a settlement is successfully reached, but costs can still add up quickly.

Choosing Between Debt Management and Debt Settlement

This decision isn’t about preference; it’s about what’s realistic and sustainable for your situation.

A Debt Management Program Is Often the More Stable Path If You:

- Have steady income and can make monthly payments

- Want to reduce interest and simplify repayment

- Are focused on limiting long-term credit damage

- Value structured support from a nonprofit agency

Debt Settlement Is Typically a Last Resort Option If You:

- Are already behind on payments or unable to stay current

- Face significant financial hardship

- Cannot realistically repay your full balance

- You are weighing options like bankruptcyweighing options like bankruptcy

How GreenPath Can Help

If you’re unsure which direction to take, you don’t have to figure it out on your own. GreenPath starts by taking a full look at your financial situation, including your income, expenses, and current debts.

From there, you’ll get clear guidance on the debt relief options available to you: what they are, how they work, and what the tradeoffs look like. If a debt management program may be a fit, GreenPath can help you understand what enrolling would involve and whether it aligns with your goals.

Together, you’ll build a personalized plan based on your financial reality, not a one-size-fits-all approach. Having empathetic, expert support can help you avoid costly missteps and move forward with more clarity and confidence.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.