Women face unique financial realities—wage gaps, caregiving responsibilities, and longer life expectancy—making intentional planning critical.

Financial confidence comes from small, consistent steps that build over time.

GreenPath’s financial counseling supports women at any stage, from budgeting and credit building to debt managementdebt management and retirement planning.

Why Financial Planning for Women Matters

Financial planning for women isn’t just about budgeting or investing—it’s about navigating real-world conditions that affect earnings, savings, and long-term security.

Women working full time in the U.S. earn about 82 cents for every dollar earned by men, according to the Pew Research Center. Over decades, this gap reduces lifetime earnings and retirement contributions.

Women are also more likely to take on unpaid caregiving responsibilities, which can interrupt income and retirement savings, as reported by AARP. When combined with longer average lifespans—women live several years longer than men—these factors make financial planning especially important.

This isn’t about capability. Women are thoughtful financial decision-makers. The key is designing a plan that accounts for income variability, longevity, and shifting life priorities. The strategies below walk through smart money moves from teens to retirement, while recognizing that every woman’s timeline is unique.

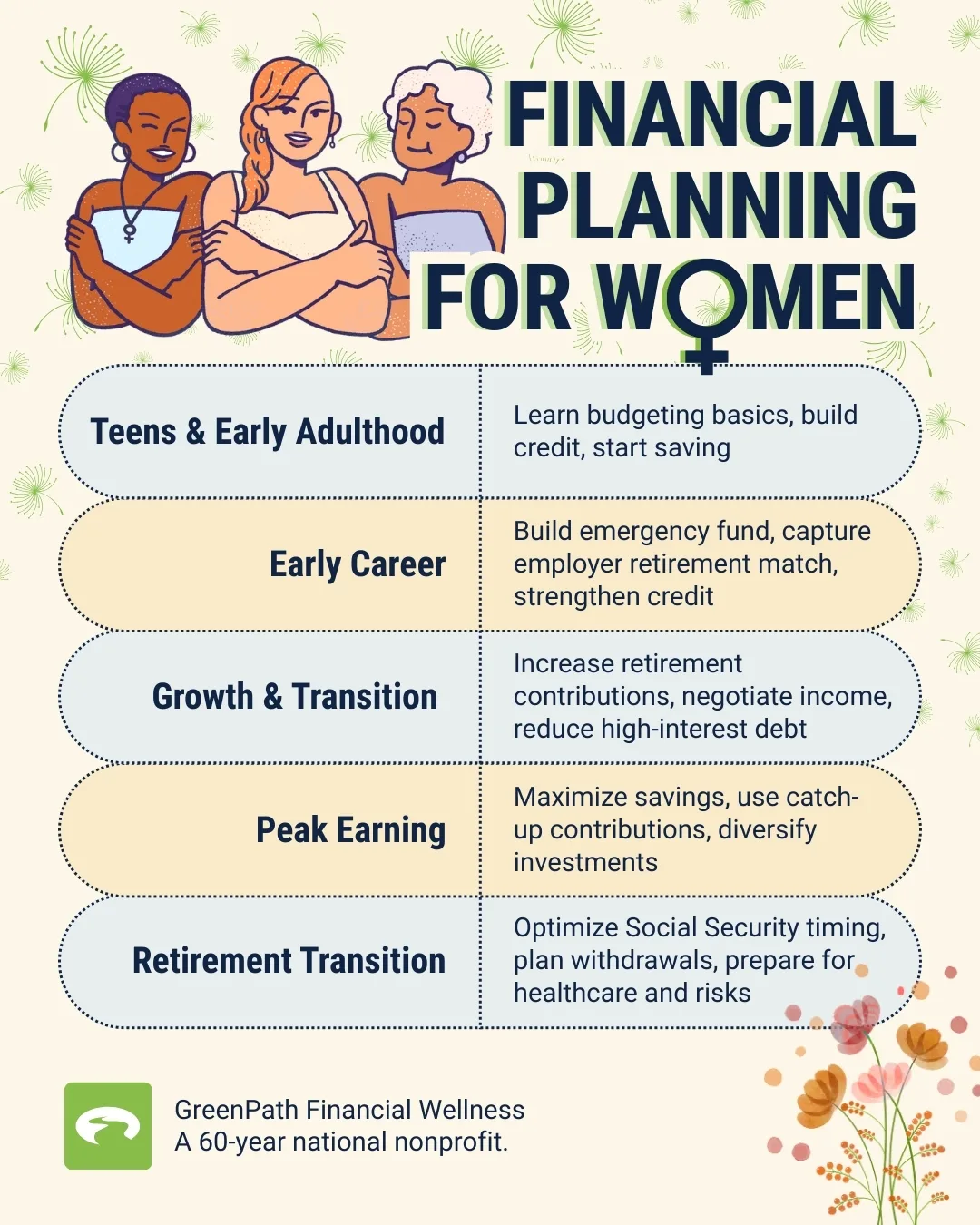

Teens & Early Adulthood: Building the Foundation

This stage is about confidence and habits, not perfection. Learning early how money flows—income, expenses, saving, and credit—gives you decision-making power throughout your life. Many people who succeed financially describe beginning with small wins like tracking spending, setting savings goals, and practicing intentional money behavior before they had big amounts to invest.

Start with clear, realistic goals: open your first checking and savings accounts so you can see how money comes and goes; learn a simple budget structure like 50% needs / 30% wants / 20% savings or debt reduction; and understand your credit (how it’s built and why it matters for loans, renting, and insurance). Paying attention now saves stress and interest payments later.

Actions:

- Treat saving like a bill. Set up a small automatic transfer right after payday. This “pay yourself first” habit helps habits stick and builds financial muscle.

- Save 5–10% of parttime income or allowances; this builds both cushion and discipline.

- Keep credit card balances low and pay on time to establish a strong credit history that can reduce borrowing costs later.

These steps help your money choices become intentional instead of impulsive, setting a foundation for healthier financial decisions in future stages.

Early Career & Financial Independence: Laying the Groundwork

Once you start earning regularly, whether that’s in your early 20s or later, financial planning becomes about systemizing your money and protecting yourself from setbacks. At this stage, building a safety net and beginning to save for long-term goals are priorities.

Financial experts recommend an emergency fund of three to six months of essential living expenses, held in an accessible account. This reserve offers security and prevents turning to high interest credit if unexpected expenses occur.

Craft a budget that reflects your lifestyle but also prioritizes saving and debt reduction. Automating transfers to savings and retirement accounts makes progress consistent, even when life gets busy. Strengthening creditStrengthening credit continues to pay off—good credit scores can reduce interest rates on loans and improve access to housing or financing.

Actions:

- Contribute at least enough to your employer’s retirement plan to capture any match; it’s a guaranteed return on your money.

- Automate savings so you “pay yourself first” before discretionary spending.

- Track your bills and payments so you never miss a due date. Timely payments are the largest factor in your credit score.

At this stage, the goal isn’t perfect saving; it’s building momentum and resilience.

Growth, Transition & Increased Responsibility

As your income and responsibilities grow, so do the financial choices you make. Whether it’s a career shift, relocation, supporting loved ones, or pursuing further education, planning strategically becomes critical. This is a stage where many women think more seriously about retirement contributions, income negotiation, debt management, and risk protection. Continued progression—even small increases in contributions or savings rates—compounds over time and strengthens long-term stability.

In this phase, it’s also common to face decisions like buying a homebuying a home or managing significant life transitions. These milestones can be powerful opportunities but also risk increasing debt if not aligned with a clear financial strategy. Prioritize reducing high interest obligations and increasing your retirement contributions when you can.

Actions:

- Target high interest debt first, like credit cards, where interest accrues most rapidly.

- Consider nonprofit financial counseling or a debt management programdebt management program if you’re juggling many payments—they can reduce rates and simplify monthly plans.

- Advocate for raises whenever appropriate; earning earlier can significantly grow your long-term savings.

This stage is about balancing growth opportunities with smart, measured planning.

Peak Earning Years: Accelerating Wealth

For many women, peak earning years come after deepening experience or overcoming earlier career interruptions. During this time, your ability to save, invest, and finetune your long-term plan can have a meaningful impact on retirement outcomes. It’s also where a thoughtful investment strategy helps keep your long-term goals on track. Experts suggest regularly reviewing your investment mix to ensure it aligns with your time horizon, risk tolerance, and income needs.

And while investment strategy is important, broad financial planning also includes insurance considerations (disability, health, life) and estate planning basics like beneficiary designations or wills. Planning ahead protects you and your loved ones from costly surprises.

Actions:

- Maximize contributions to tax advantaged accounts and take advantage of any age based catchup options available (typically starting at age 50).

- Rebalance your portfolio at least annually to stay aligned with your goals.

- Maintain adequate insurance—sudden loss of incomesudden loss of income or major healthcare needs can derail a financial plan if you’re unprotected.

Approaching this stage with intention can accelerate your wealth and create a stronger financial foundation for retirement.

Retirement Transition & Income Planning

Retirement planning for women must account for longevity and income sustainability. Women tend to live longer than men, increasing the need for a retirement plan that lasts decades. Research also shows many women save less for retirement than men, and a significant share skip retirement contributions altogether—missed opportunities that compound over time.

When you’re approaching or already in retirement, it’s crucial to look beyond just savings totals and focus on income strategies: when to claim Social Security, how to sequence withdrawals, and how to manage healthcare costs. A holistic approach—considering guaranteed income sources and market investments—helps sustain income throughout retirement.

Actions:

- Evaluate optimal Social Security timing: delaying benefits up to age 70 can increase monthly income and longevity protection.

- Build a sustainable withdrawal plan that balances lifetime income needs with investment growth.

- Plan for healthcare costs, including Medicare premiums and supplemental insurance, which are common retirement expenses.

Even small, informed decisions in this stage can significantly reduce financial stressreduce financial stress and preserve your lifestyle.

Emotional Realities Across Life Stages

Many women experience financial anxiety, guilt about spending, or shame around debt. These feelings are common and not a reflection of competence.

Confidence grows through measurable progress, such as:

- Increasing savings each month

- Reducing debt balances consistently

- Incrementally raising retirement contributions

Financial planning is about progress, not perfection.

How GreenPath Supports Women Through Every Financial Chapter

GreenPath provides free financial counselingfree financial counseling tailored to your stage of life:

- Personalized budgeting strategies

- Credit review and improvement guidance

- Debt management programs that may reduce interest and simplify payments

- Housing and foreclosure prevention support

You don’t have to navigate these challenges alone. GreenPath helps women build a roadmap to long-term security—at every stage.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.