You don’t need perfect timing or huge deposits to build savings. Small, automated moves—done consistently—create momentum that survives price spikes and surprises.

Where you save matters. Parking cash in the right accounts and shrinking high-interest debthigh-interest debt can quietly free up more money without changing your lifestyle.

If your budget feels tight, it’s not a personal failure—it’s a signal. Updating your plan to reflect today’s costs reduces stress and restores control.

Small Systems Win

If you’re reading this, there’s a good chance you tried the “New Year, new savings goal” thing before—and life, inflation, or a surprise bill had other plans. You’re in good company. According to NerdWallet’s 2026 Consumer Outlook Report, more than half of Americans expect prices to keep climbing in the year ahead.

When costs feel unpredictable, saving can start to feel less like a goal and more like a gamble—especially if you’ve been burned before.

Building savings doesn’t have to rely on willpower, perfect timing, or one big, make-or-break resolution. Instead, the most resilient savers focus on small, repeatable systems that work with real life—not against it. Systems that keep moving forward even when prices zigzag or plans change.

Below is a step-by-step, no-shame playbook to help you do exactly that.

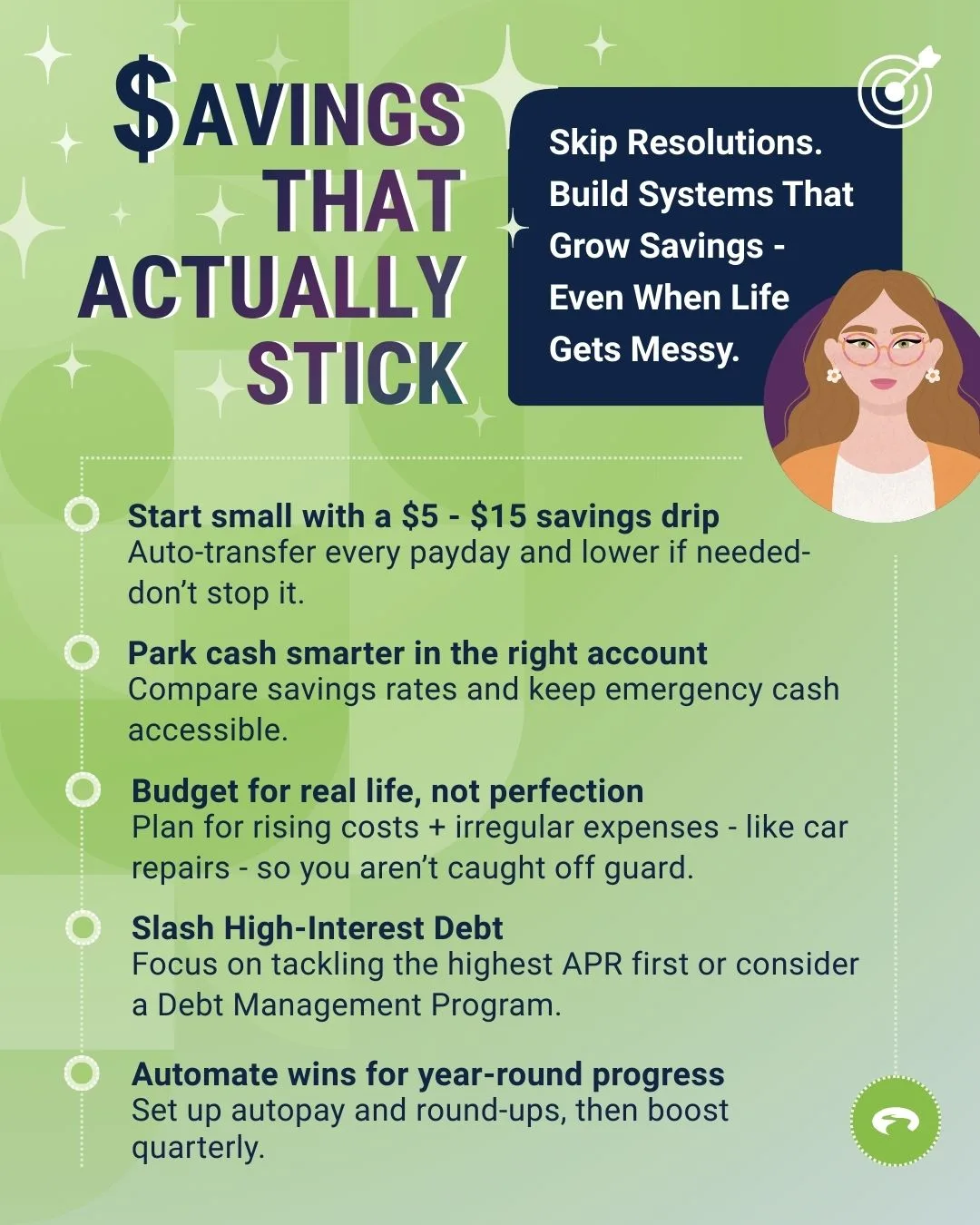

1. Start Micro: A $5–$15 “Savings Drip”

Why it works: Psychologically, microtransfers keep momentum without triggering scarcity—especially when groceries, utilities, and insurance premiums are doing their own thing.

How to do it today

- Auto transfer $5–$15 every payday to a separate savings account you don’t touch.

- Label it “Safety Net” in your banking app. Visual cues help.

- When budgets feel tight, lower the drip—don’t stop it.

Pro Tip

Put the drip in a high-yield savings account (HYSA) so your dollars earn more while you sleep. Many HYSAs still pay several times the national average—despite recent Fed rate cuts—so it’s low effort, real gain.

2. Park Cash Where It Grows (Not Where It’s Convenient)

If your savings is sitting where it’s always been, that’s understandable. Most of us opened an account once and moved on—because life got busy. But over time, “set it and forget it” can quietly cost you.

Making your savings work harder doesn’t require taking risks or changing habits. It usually just means checking whether your money is parked in a place that still serves you.

Your quick action

- Take a few minutes to compare savings rates at online banks or credit unions. Moving an emergency fund can feel like a hassle—but it’s often a one-time switch that pays you back every month.

- If part of your savings won’t be needed for 6–12 months, consider a laddered CD for that portion to lock in a rate—while keeping at least one month of expenses fully liquid for peace of mind.

3. Budget for the Reality You Feel

Think your budget is fine—but your wallet disagrees? You’re not imagining it. Everyday costs add up faster than most budgets anticipate. In 2025, the average monthly grocery spend in the U.S. is roughly $665 per person (and in many states it’s even higher).

A realistic budget isn’t about discipline or deprivation. It’s about updating your plan so it actually works for your life today.

Try this 20-minute refresh

- List the “movers.” Identify the categories that quietly crept up this year and now take more of your paycheck.

- Right-size with compassion. Increase caps where costs are unavoidable—and trim areas you’re no longer using or valuing, like forgotten subscriptions or unused memberships.

- Pre-fund the surprises. Set aside a little each month for irregular but predictable costs (car repairs, copays). When they hit, they’ll feel less like emergencies.

- Be selective with rewards. Cash back and points only help if balances are paid in full. Otherwise, interest quickly outweighs any perks.

A budget that acknowledges reality—rather than fighting it—gives you more control and a lot less stress.

4. Triage High-Cost Debt First

Credit card delinquencies and balances climbed from pandemic lows and remain elevated, signaling stress for many households. If minimums feel like quicksand, tackling interest is the fastest way to free cash for savings.

Your options

- Snowball/Avalanche: Pay smallest balance or highest APR first—whichever keeps you consistent.

- Ask for an APR reduction: A five-minute call can lower a rate, especially if you’ve been on time.

- A Debt Management ProgramDebt Management Program can roll multiple cards into one payment and often secure lower interest rates from creditors, cutting stress and helping you rebuild savings sooner.

5. Automate the “Boring” Wins

You don’t need to overhaul your life to make progress. Setting up simple systems that quietly build savings can be more effective than occasional big leaps.

- Bill calendar + autopay for essentials to avoid late fees and protect your creditprotect your credit profile.

- Roundups: Enable roundup transfers (or a weekly $10 sweep) to your HYSA.

- Quarterly check-in: Every three months, raise your savings drip by $5—small enough to feel easy, meaningful over a year.

6. Don’t Wait for Certainty

The perfect moment rarely comes—so start anyway. Life is unpredictable. Instead of waiting for ideal circumstances, plan around them and build security over time.

- Keep 3–6 months of essential expenses as the target over time (not overnight).

- Split savings: 80% emergency fund / 20% “future you” (home maintenance, car, medical).

- If your income is variable, build a one month “buffer” first (rent/mortgage + groceries + utilities), then expand.

Simple Swaps That Save

- Swap brands and stores, not meals: Same recipes, different labels (or warehouse club for staples) can shave 10–15% off grocery bills.

- Utility “nudges”: Smart thermostat schedules and LED swaps lower monthly costs with one-and-done changes.

- Insurance shopping: Quote home/auto annually; bundling or usage-based programs often save 5–10%.

- Library and local perks: Free streaming, museum passes, and workshops can replace paid services.

With GreenPath, There’s a Plan for Every Dollar

When every paycheck seems to disappear into high balances or sky-high interest rates, it can feel like there’s never enough to cover what matters most. GreenPath’s NFCC-certified counselors are here to listen, guide, and help you find clarity—completely free and confidential. Together, you’ll explore your options, create a plan that fits your life, and take realistic steps toward easing financial stress.

And if high balances or sky-high interest rates are making it feel like there’s never enough to cover what matters most, our Debt Management Program (DMP)Debt Management Program (DMP) can help. By lowering interest and simplifying payments, it turns today’s pressure into room to save, plan, and regain control of your finances.

You Might Also Be Interested In…

Webinar: Setting and Reaching Goals in 2026 Setting and Reaching Goals in 2026

What You Will Learn

- How to set realistic goals that can actually be achieved

- The role financial habits play in reaching (or abandoning) your financial goals

- How to get back on track after a setback

GreenPath Financial Service

GreenPath, A Financial Resource

If you’re interested in building healthy financial habits, paying down debt, or saving for what matters most, take a look at these free financial tools.