A credit score drop is usually tied to a few common triggers (like higher card balances, a missed payment, or a new application)—and most are fixable with a simple plan.

One of the fastest ways to stabilize your score is lowering your reported credit card balances, because that can update with your next statement cycle.

If your score drop is tied to debt stress or staying on top of payments, GreenPath’s free virtual financial coachGreenPath’s free virtual financial coach can help you understand what’s happening and map out next steps—privately, on your schedule, and without pressure.

What It Means When Your Credit Score Drops

A credit score dipcredit score dip can feel surprisingly emotional, like a setback or a judgment, even when you’re doing your best to stay on top of things. But much of the time, it’s simply your credit report updating with new information (such as a higher balance being reported, or a lender checking your credit after you applied), not a reflection of your financial instincts.

It helps to know that you don’t have just one score. Different lenders may use different scoring models and versions, so you can see slightly different numbers depending on where you check.

Score movement is normal, even nationally. Experian reports the average U.S. FICO® Score declined to 713 in 2025 (down from 715 in 2024). That doesn’t make your drop any less annoying, but it does reinforce this: score changes happen, and they can happen to anyone.

Is This a Small Dip…or a Bigger Red Flag?

Before you start “fixing” things, take 2 minutes to figure out what kind of drop you’re dealing with.

A small dip (often temporary)

Usually 5–20 points, often tied to:

- A higher reported credit card balance (even if you pay in full later)

- A hard inquiry from a new application

- A new account lowering your average account age

- Paying off a loan (yes, sometimes this can cause a small dip)

A bigger drop (investigate ASAP)

Often 20+ points, more commonly tied to:

- A missed payment that hit 30+ days late

- A big jump in credit card balances (higher utilization)

- A collection account

- A reporting error or identity theft concern

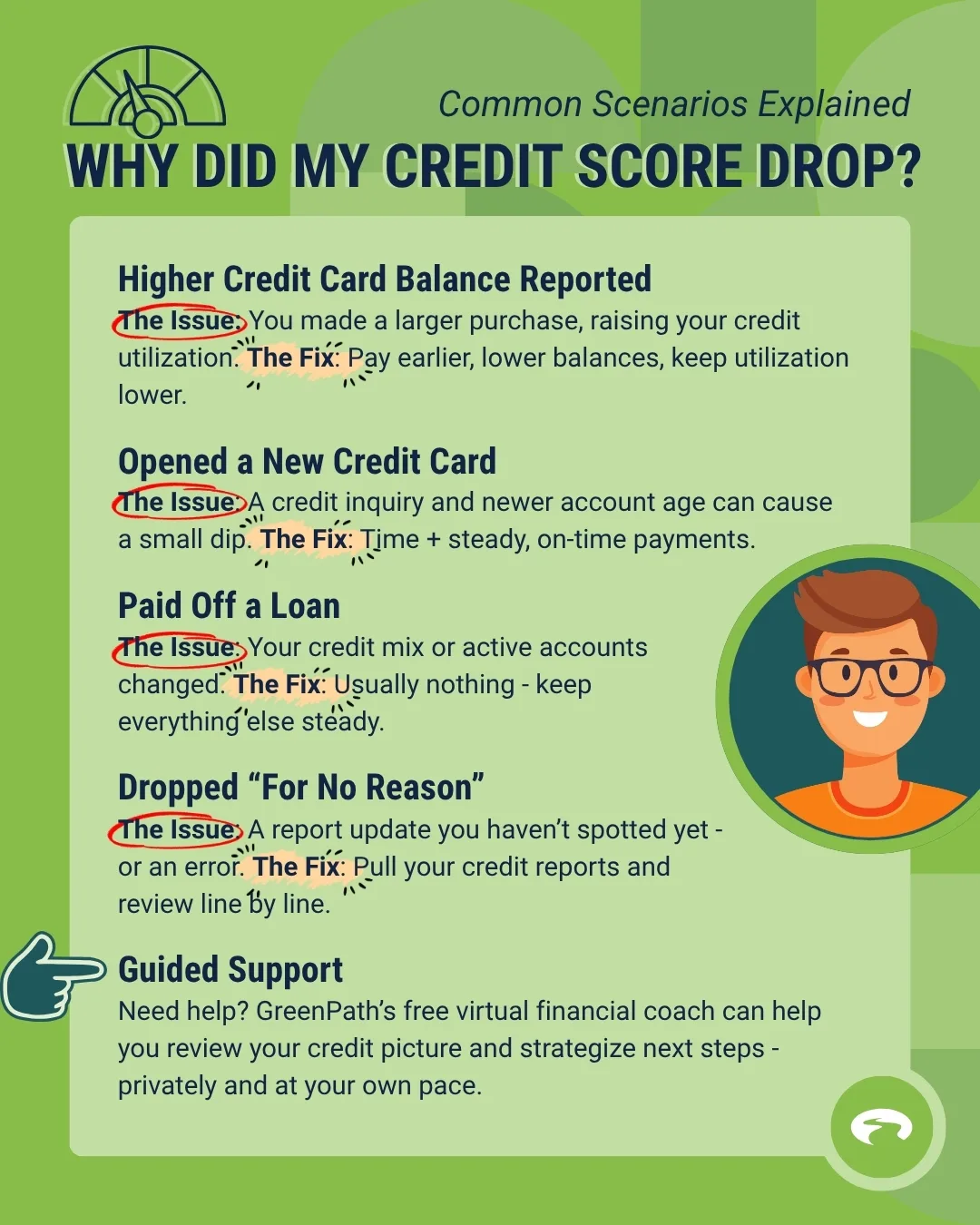

1. Your credit card balance reported higher than usual (even if you pay in full)

This is a sneaky one, because it can happen even when you’re doing everything “right.”

Your card issuer typically reports a balance to the credit bureaus around your statement closing date. If your balance is higher at that moment (due to travel, a big purchase, or just a spendy month), your credit utilization can go up—and your score can dip.

Helpful benchmark: Experian reports average credit card utilization was 29.1% in September 2025, and notes that around 30% is where utilization starts to have a greater negative effect on credit scores.

Example:

- You have a $10,000 limit.

- Last month, your statement closed at $800 (8% utilization).

- This month, it closed at $3,200 (32% utilization).

That 32% snapshot can show up on your credit report, even if you pay the card off a week later.

What to do:

- Pay before your statement closes (not just by the due date), so the reported balance is lower.

- Work toward more breathing room by paying balances down and keeping utilization comfortably below that ~30% range when you can.

- If you have multiple cards, avoid running one card high if another has room.

2. You missed a payment (or paid 30+ days late)

A late payment that crosses 30 days past due can show up on your credit report and hurt your score more than people expect.

Example:

You forgot a store card you rarely use. The minimum payment was $29. It becomes 30 days late and your score drops even if everything else is spotless.

What to do:

- Get current immediately (pay what’s past due).

- Set up autopay for at least the minimum on every account (especially “set it and forget it” cards).

- If this is not a pattern and you’ve usually paid on time, call and ask for a goodwill adjustment (not guaranteed, but worth trying).

3. You applied for new credit (hard inquiry) or opened a new account

When you apply for credit, a lender may run a hard inquiry, which can cause a small, short-term dip. Opening a new account can also lower your average account age.

Example:

You open a new rewards card. Your score dips a bit due to the inquiry + the new account.

What to do:

- If you’re planning a big loan soon (mortgage, auto), limit new applications in the months leading up.

- If you are rate-shopping for a car loanrate-shopping for a car loan, do it in a tight window so your inquiries are more likely to be treated as a single shopping period by scoring models (varies by model).

4. You closed a credit card (or a card was closed for you)

Closing a card can reduce your total available credit. That can push your utilization up, even if your spending didn’t change.

Example:

- Two cards, each with a $5,000 limit.

- One has a $2,000 balance.

- With both cards open: $2,000 / $10,000 = 20% utilization.

- Close one card: $2,000 / $5,000 = 40% utilization (and your score may drop).

What to do:

- If a card has no annual fee, consider keeping it open, especially if it’s older.

- If you need to close a card, try to pay down other balances first, so utilization doesn’t spike.

5. You paid off a loan—and your score dipped anyway

This feels unfair, but it can happen. Paying off an installment loan can change your “credit mix” or reduce the number of active accounts reporting, which may cause a short-term dip.

Example:

You pay off a car loan? Huge win. Next month, you notice a small score drop. Often it stabilizes as you continue paying other accounts on time.

What to do:

- Nothing. Keep making on-time payments and keep credit card balances manageable.

6. A collection account appeared (medical bill, old utility bill, etc.)

Collections can cause a meaningful score drop and can affect approvals.

What to do:

- Confirm it’s yours and request details in writing.

- If it’s legitimate, explore options for resolving it, and keep records of any agreement.

7. Your credit report has an error—or identity theft is involved

Sometimes the reason is simple: your report is wrong, or a fraud issue needs attentiona fraud issue needs attention.

Errors can range from inaccurate balances to accounts you don’t recognize, and they’re more common than many people realize.

That’s why it’s important to review your credit reports regularly. You can get at least one free credit report each year from each of the three major credit bureaus by visiting AnnualCreditReport.com. Checking your reports can help you spot problems early and take action before they cause lasting damage.

What to do:

- Look for accounts you don’t recognize, incorrect balances, or late payments that don’t match your records.

- Dispute inaccuracies promptly with the credit bureau(s) and the company reporting the information.

- If fraud is suspected, consider tools like a fraud alert or credit freeze right away.

Your Score Is Feedback, Not a Verdict

If your credit score dropped because of higher balances or missed payments, it’s not a personal failure; it’s often a reflection of how quickly everyday costs can add up. Credit score changes are signals, pointing to something on your credit report that shifted.

This is where GreenPath’s free virtual financial coachGreenPath’s free virtual financial coach can help. It provides an easy, private way to understand why your credit score dropped, review what’s shown on your credit report, and identify realistic next steps to improve your financial situation.

For those who want additional guidance, GreenPath also offers free, confidential financial counselingfree, confidential financial counseling. A lower credit score can feel discouraging, but it’s also actionable information. Once you identify the cause—whether it’s credit utilization, a missed payment, a new account, or an error on your credit report—you can move forward with a plan instead of uncertainty.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.