Your Flexible Spending Account doesn’t last forever — unused funds can disappear if you don’t act before your plan’s deadlines.

The IRS allows carryover (or grace period) options, but only up to certain limits and only if your employer offers them.

Worried about leaving money on the table? GreenPath can help you assess your budgetassess your budget to avoid future waste.

If you’ve been putting money into your Flexible Spending Account (FSA) all year, well done! Flexible spending accounts are special spending accounts that allow employees to pay for eligible healthcare and dependent care expenses using pretax dollars.

As the year-end nearsthe year-end nears, don’t forget: many of those FSA dollars expire soon. If you don’t use them (or submit eligible claims), the “use-it-or-lose-it” rule could cost you real cash. Let’s walk through what to watch for and how to squeeze every cent out of that account.

Flexible Spending Accounts Deadlines & Rules

First off, check with your employer or benefits portal to see whether your FSA has a carryover, a grace period, or neither. Every plan is a little different—but here’s the general IRS-level framework:

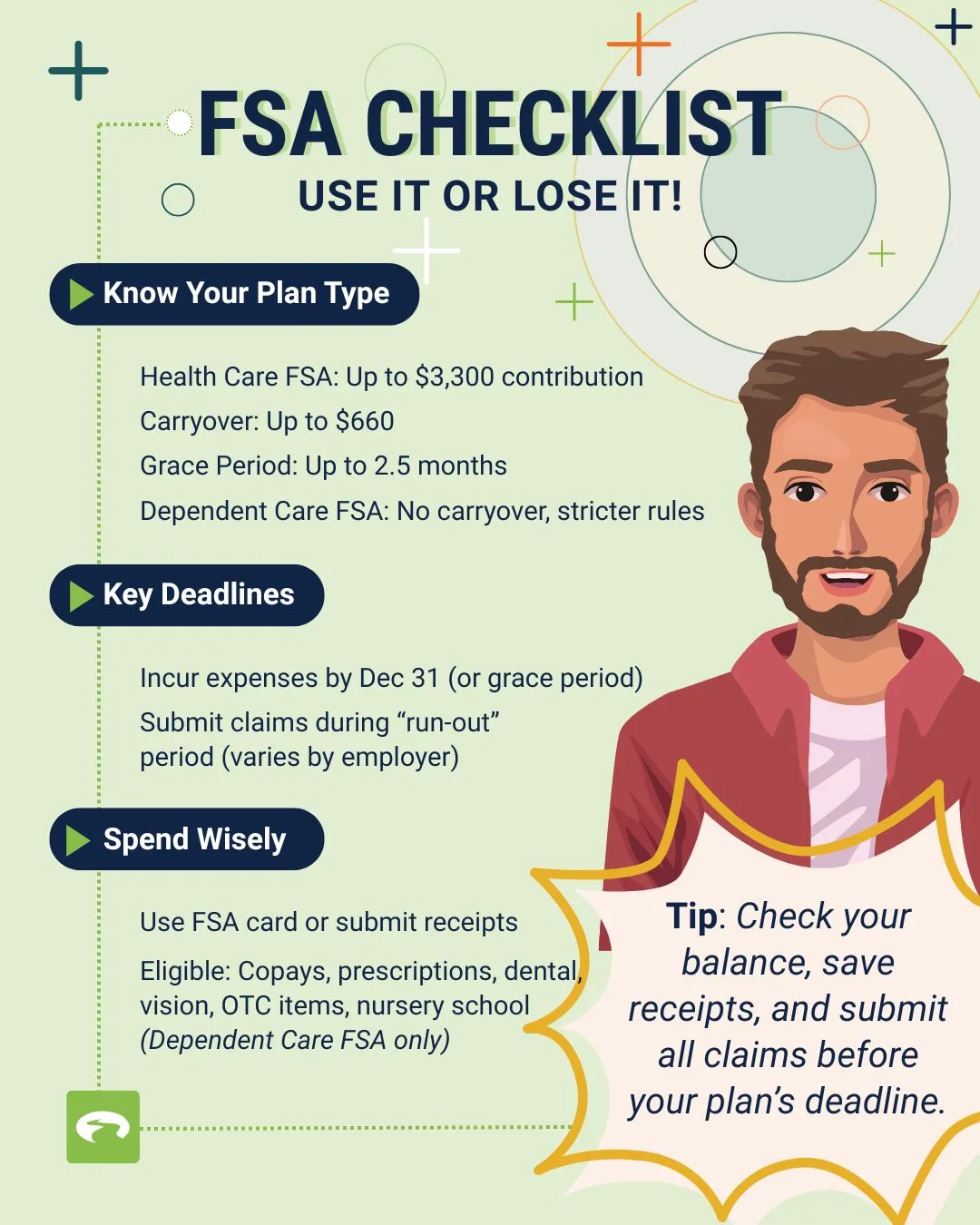

- For the 2025 plan year, the IRS states you may contribute up to $3,300 to a health-care FSA.

- The maximum carryover amount for Health Care FSA (if your plan allows it) is up to $660 for 2025.

- Some plans instead offer a grace period, such as up to 2½ months after plan-year end (commonly until March 15), during which you can still “spend down” your remaining balance.

- Other plans require you to incur eligible expenses by December 31 with a “run-out period” afterward to file claims. The length of the run-out period is set by your employer and may vary.

- You may not be able to use your FSA debit card during the grace period, depending on your plan administrator. Manual claims may be required.

- IRS regulations require you to make an annual election for your FSA during open enrollment, and you may need to re-enroll each next plan year to continue your benefits. Only qualified expenses incurred during the plan year, grace period, or run-out period qualify for reimbursement, and you must submit a claim for these expenses before the deadline.

- If you leave your job, you typically lose access to incur new expenses, but you may still submit claims for expenses incurred before termination during the run-out period. COBRA continuation may be available for health FSAs if you have a positive balance.

Because of these variations, it’s wise to familiarize yourself with your own plan’s rules before December.

Why It Matters (Especially Around the Holidays)

- Many of us schedule dental cleanings, vision exams, prescriptions, or even medical supplies toward the end of the year — and FSA funds can cover those. Examples of qualified medical expenses and healthcare expenses you can pay for with your FSA include out-of-pocket expenses like copays, deductibles, prescription medications, and certain over-the-counter items.

- You can pay for eligible expenses directly by using a debit card linked to your FSA, or by paying out of pocket and then requesting reimbursement through direct deposit for faster access to your funds.

- If you don’t use your FSA money now, you could miss out on tax-savings you’ve been banking all year.

- Unused FSA dollars don’t usually roll over indefinitely — they’re time-sensitive, unlike HSAs.

Plus, with holiday spendingholiday spending on gifts, travel, or unexpected expenses, it’s easy to get distracted. But your FSA is a built-in “free money” for health needs — don’t let it slip away

What to Do Right Now Before the Plan Year Ends

| Check your FSA summary online | See how much balance remains, when your “incurred by” deadline is, and when you must submit receipts/claims. |

| Review upcoming medical or health costs | Do you have upcoming co-pays, prescriptions, dental, vision, or over-the-counter health needs? Many OTC medicines and medical supplies are eligible for reimbursement. |

| Place eligible orders now | Some eligible items (OTC wellness products, first-aid supplies, etc.) can be bought ahead of time. Keep receipts. |

| Plan for your “run-out” or “grace period” submission | Know your final date to spend (incur expenses) and to submit claims. Don’t fake it — late claims are often rejected. |

| Document carefully | Save receipts, check for eligible expenses (even small ones), and track what’s reimbursed. Document all claims and reimbursements, including dependent care expenses such as nursery school costs. |

Also, if you have more than one FSA (health care FSA, dependent care FSA, limited-purpose FSA), each may have different rules — take a quick inventory of all of them.

- Dependent care claims must be incurred during the plan year or grace period, and reimbursements are limited to the amount contributed at the time of claim.

- You can submit claims for eligible expenses covered by your FSA — such as medical, dental, vision, and over-the-counter health items for a Healthcare FSA, or childcare and nursery school costs for a Dependent Care FSA. Approved reimbursements are typically issued by direct deposit or check once your claim is processed.

When Your FSA Eligible Expenses Rules Get Tricky

- Carryover vs. Grace Period

These rules apply specifically to a healthcare FSA (also known as FSA healthcare). Your employer may offer one or the other, or in rare cases, neither. If you have carryover, leftover dollars up to the IRS limit can move forward. If you have a grace period, you may have a few extra months to spend on services that occurred before Dec 31. But you typically can’t have both. - Dependent Care FSA

Often, dependent care FSAs have stricter rules or don’t allow carryover—even when your health-care FSA does. Make sure you check what types of FSA you’re dealing with. - Leaving your job or changing your benefits plan

Some carryover or run-out protections depend on you still being eligible or still employed under the same health plan. If you anticipate changes in employment or benefit status next year, double-check how that affects your FSA and any other spending accounts you may have. - Underusing small-ticket purchases

Over-the-counter items (first-aid supplies, prescriptions, wellness tools, etc.) can often be eligible — even things you didn’t immediately think about earlier in the year. It’s common to leave small dollars unspent because people forget they can use FSA for them. These small-ticket purchases can help you use funds remaining in your account before deadlines. - Comparing account types

A healthcare FSA is a type of spending account that lets you use pre-tax dollars for eligible medical expenses, but funds remaining at year-end may be forfeited unless your plan allows carryover or a grace period.

In contrast, a health savings account (HSA) is only available with a high-deductible health plan, allows you to keep all unused funds year to year, and offers additional tax advantages. Some dependent care expenses may also qualify for a tax credit, which directly reduces your tax liability, unlike pre-tax deductions from spending accounts.

How GreenPath Can Help

If you find that you’ve misestimated your expenses, or you’re juggling multiple benefit-account deadlines alongside credit card balances, monthly bills, or holiday spending plans, don’t hesitate to seek support.

GreenPath offers free financial counselingfree financial counseling that can help you review your budget (including FSAs, medical spending, credit card balances, and more), plan for your upcoming year, and avoid waste like unused FSA dollars.

GreenPath Financial Service

GreenPath, A Financial Resource

If you’re interested in building healthy financial habits, paying down debt, or saving for what matters most, take a look at these free financial tools.