A mid-year financial check-in helps you assess, organize, and improve your financial health.

Steps like budgeting, strategizing debt payoffdebt payoff, and automating payments can lead to big savings.

Use this checklist to reduce money stress and finish the year financially stronger.

Why a Mid-Year Financial Cleanse Matters

When you hear the word “cleanse,” you might think of juice detoxes or closet cleanouts—but have you considered a financial cleanse?

Now that we’ve hit the midpoint of the year, it’s a great time to declutter your money habits, recheck your progress, and build a plan that aligns with your goalsaligns with your goals—whether it’s tackling debt, saving more, or simply getting organized. Use this 10-step checklist to streamline your finances and reset with intention.

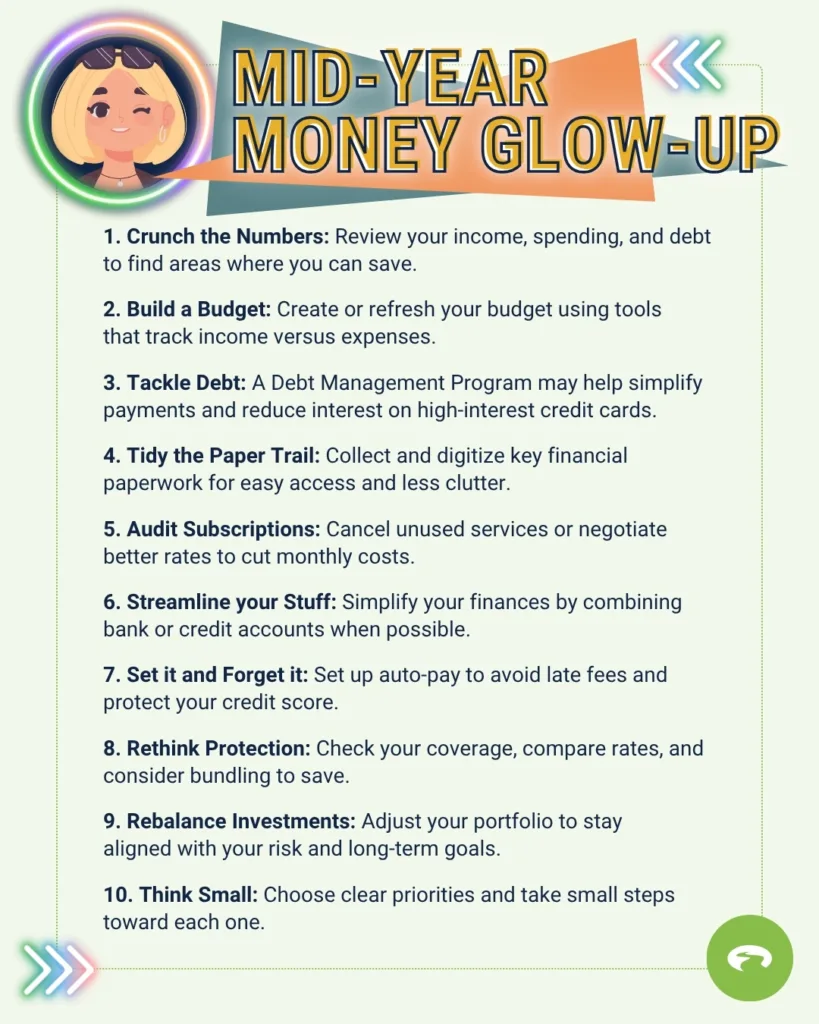

1. Think Big Picture: What Does Your Current Financial Landscape Look Like?

Before you tackle a messy room, it helps to know what you’re getting into first. A budget works the same way—it starts with awareness. Begin your mid-year financial review by assessing your overall financial situation. Look at your bank statements, credit card statements, and other financial documents to better understand your income, expenses, and debt. Are there areas you can trim? Maybe you’re overpaying on auto insurance, cable, or internet—a little comparison shopping or rate negotiation could reveal big savings.

2. Build a Budget That Reflects Your Life and Goals

Whether you prefer spreadsheets, money management apps, or an interactive budgeting worksheetinteractive budgeting worksheet, the how is less important than the why. And here’s the why: a budget is one of the most effective tools to stay organized, track spending, and gain peace of mind. Review your current budget or build a new one if you’re starting fresh. Include specific categories for your income, fixed expenses, and variable costs, and try to allocate even a small amount toward savings or emergency funds. This is how you prepare for the unexpected and avoid added stress down the line.

3. Tackle Your Debt Strategically

Start by listing your outstanding debts, interest rates, and monthly payments to get a clear picture of what you owe. Then consider your options—especially if you’re only making minimum payments and struggling to make a dent. A Debt Management Program (DMP)Debt Management Program (DMP) is designed to help you lower interest rates, combine multiple payments into one, and pay off debt faster—without taking on new loans.

4. Organize Your Financial Documents (Yes, It’s Worth It!)

Gather and organize important financial paperwork like tax returns, bank statements, investment records, insurance policies, and receipts. A simple filing system—physical, digital, or both—ensures easy access when you need to reference what your renter’s insurance covers or when a promotional 0% interest rate ends. Digitizing your documents also frees up space and reduces stress. Think of it as a financial and physical decluttering session all in one.

5. Optimize Subscriptions and Monthly Memberships

Mid-year is a great time to do a subscription audit. What are you paying for monthly that no longer adds value? Maybe that streaming music service or meal kit delivery isn’t as essential as it once was. On the flip side, your gym membership or meditation app might be worth every penny. It all depends on your current priorities. Cancel subscriptions you don’t use, negotiate better rates, or switch to more affordable alternatives to save money without sacrificing quality of life.

6. Consolidate and Simplify Financial Accounts

Too many accounts can create unnecessary stress. If you have multiple checking or savings accounts at different institutions, consider consolidating to simplify money management, reduce maintenance fees, and better track your financial goals. Similarly, combining credit card balances onto one lower-interest card can streamline payments and potentially lower your overall interest charges. The simpler your financial setup, the easier it is to monitor your progress.

7. Automate Your Bill Payments to Avoid Late Fees

If managing bills gives you anxiety, you’re not alone. Forgetting a due date can lead to late fees or even credit score damagecredit score damage. The solution? Set up automatic bill payments for recurring expenses like rent, utilities, loans, and credit cards. Automation not only protects your budget and your credit—it also frees up mental energy for more important financial planning.

8. Review and Update Insurance Policies to Maximize Coverage and Savings

Insurance isn’t something you want to “set and forget.” Take time to review your home, auto, health, renters, or life insurance policies. Are you still getting the best rates? Could you bundle and save? Are you paying for coverage you no longer need? Compare quotes, adjust deductibles, and confirm your coverage aligns with your current lifestyle and assets. Small updates can mean big savings—and better peace of mind.

9. Review and Rebalance Investments for Long-Term Success

If you have a 401(k), IRA, or other investments, now’s the time to review their performance and make sure they’re aligned with your risk tolerance and long-term goals. Consider rebalancing your portfolio to maintain diversification and optimize returns. If you’re unsure how to assess your portfolio’s health or rebalance wisely, a certified financial advisor can walk you through it. Regular check-ins are key to growing wealth over time.

10. Set Mid-Year Financial Goals to Finish Strong

The middle of the year is a natural time to reflect and reset. What do you want to accomplish financially in the next six months? Whether it’s saving for a vacation, paying off credit card debt, or starting a retirement contribution, define your priorities and break them down into small, achievable steps. Big goals are reached through consistent effort, and even small wins move you forward.

You Might Also Be Interested In…

GreenPath Financial Service

GreenPath, A Financial Resource

If you’re interested in building healthy financial habits, paying down debt, or saving for what matters most, take a look at these free financial tools.