A Debt Management Program (DMP) can simplify repayment by combining payments and lowering interest rates and fees.

There may be short-term trade-offs, like closing credit cards or a temporary credit score dip, but most people see long-term financial improvements.

GreenPath’s DMP provides a structured, supportive path to pay off debt faster while building healthier financial habits over time.

Thinking About a Debt Management Program? Start Here.

Maybe you’ve been making payments but not seeing the balance budge. Or one expense turned into a balance that’s now hard to ignore. However you got here, if you’ve started looking into a Debt Management ProgramDebt Management Program, you’ve probably also got a list of questions.

That’s a good thing! The more you understand your options, the more confident you’ll feel moving forward. Let’s walk through the most frequent questions together.

What is a Debt Management Program and how does it work?

A Debt Management Program (DMP) is a structured plan offered by nonprofit credit counseling agencies, such as GreenPath, to help individuals pay off unsecured debts through a single, manageable monthly payment.

Each payday, you deposit funds into a secure GreenPath account, and we pay your creditors on your behalf.

Who is eligible for a DMP?

The DMP is designed for people with unsecured debtunsecured debt, such as credit cards, department store cards, medical bills, or personal loans, and the program is tailored to your unique financial situation.

A DMP can be a smart solution for those struggling with high-interest credit card debt. It’s especially valuable if you’re:

- Making only minimum payments and not seeing progress

- Juggling multiple credit card accounts

- Facing mounting interest that makes it hard to pay off balances

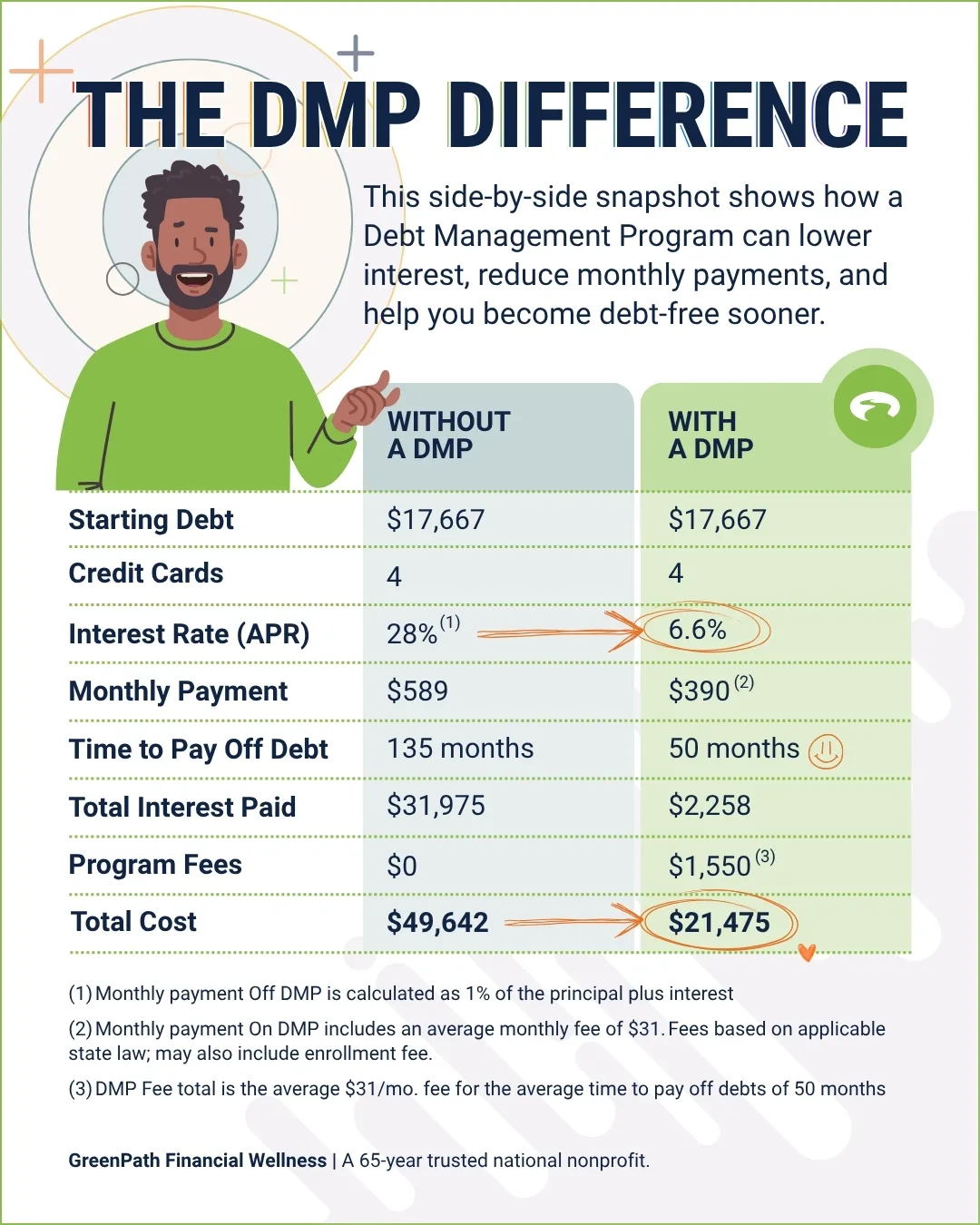

How much could I save on a DMP versus repaying debt on my own?

While every situation is different, many people see meaningful savings with a DMP. For the average DMP client:

- Interest rates can drop from about 28% to 6.6%, helping more of each payment go toward your balance

- Monthly payments decrease by about $199

- Interest savings add up to roughly $29,700 over time

- Debt is paid off faster (about 7 years sooner)

How do I know a DMP isn’t a scam?

GreenPath is a trusted national nonprofit. Since 1961, we’ve helped households across the country repay billions of dollars in debt. We don’t work for banks, but we do partner with more than 650 banks, credit unions, and employers nationwide. Creditors often support DMPs because they see the results: people repaying debt in a manageable way that leads to long-term stability.

How much does it cost for a debt management program?

DMP setup fees and monthly fees vary based on your state of residence and debt amount. On average, GreenPath clients are charged a one-time enrollment fee of $35 and a $31 monthly fee. This is minimal considering the amount of money our clients typically save in waived late fees, waived over limit fees, and reduced credit card interest charges.

Do I have to sign a contract if I begin a debt management program?

There is an agreement you will sign when starting a DMP. The agreement specifies program details and gives us permission to pay creditors on your behalf. The agreement is not binding, and you can cancel the program at any time.

Will enrolling hurt my credit score?

GreenPath does not report to credit bureaus (Experian, TransUnion, or Equifax). You may see a temporary dip at first, especially as accounts close.

Over time, many people see improvement. Consistent, on-time payments and decreasing balances are positive signals your credit history will reflect.

Are debt management programs different from debt settlement?

Yes. Debt management programs are designed to pay off the entire amount you owe in 3 to 5 years. If we can lower your interest rates, the total amount you pay to your credit card company is typically less than if you paid on your own.

Debt settlement typically involves requesting credit card companies to forgive a portion of your debt in exchange for a lump sum payment. Be sure to understand the risks of debt settlementunderstand the risks of debt settlement if you’re considering this option.

What is the difference between debt management programs and debt consolidation?

A DMP is set up through a nonprofit credit counseling agency like GreenPath. Instead of taking out a new loan, your existing debts are included in a structured repayment program. Your creditors may agree to lower interest rates and fees, and you make one consistent monthly payment based on what fits your budget.

Debt consolidationDebt consolidation typically means taking out a new loan (or using a balance transfer card) to combine multiple debts into one. While this can simplify payments, it doesn’t always reduce interest rates—and approval often depends on your credit score.

Can I keep some credit card accounts open?

Since the goal of a DMP is to eliminate your debt, this process begins with closing the credit cards included in your program. If you need to keep one card for emergencies or business, we can evaluate your options together.

What is a proposal?

A proposal is a document sent to your creditors requesting adjusted terms—like a new payment amount, lower interest rate, or other concessions.

It’s what helps make repayment more manageable by aligning your accounts into a more consistent structure.

What are concessions?

Concessions are the adjustments creditors may agree to, such as reduced interest rates, extended repayment periods, or waived fees.

These changes are a big part of what makes a DMP effective—lowering costs and making payments more predictable.

How long will the program take?

Contracts are typically for the maximum period allowed by the state (60 months). Early completion due to creditor concessions will successfully close your DMP.

Still have questions? Let’s talk.

You can connect with HUD- and NFCC-certified GreenPath counselors during business hours for a free, confidential consultation and also check out our FAQ page.FAQ page.

And if you’re already enrolled in GreenPath’s DMP, you have access to a private online community where people share advice, ask questions, and support each other along the way.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.