Debt Settlement Risks: What to Know Before You Enroll

Debt settlement may seem like a quick fix, but it can damage your credit, trigger collections, and cost more than expected.

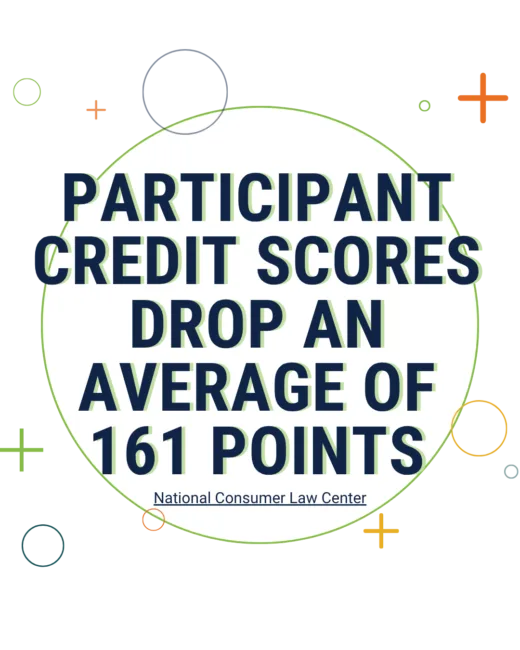

Debt Settlement Can Severely Damage Your Credit

Most debt settlement programs require you to stop making payments while negotiations take place. Missed payments can stay on your credit report for years and may significantly lower your credit score.

Accounts reported as “settled” instead of “paid in full” may also signal financial distress to future lenders.

Key Risks

- Missed payments hurt your payment history

- Credit scores can drop significantly

- Late fees and penalty interest may continue growing

- Settled accounts may remain on your credit report for years

How Much Debt Do You Owe?

Use this calculator to see how much it would cost to settle your debt.

$1

$100K+

Debt Settlement Can Be Costly

- Fees are typically 15–25% of enrolled debt.

- During the process, companies may hold client funds while waiting for accounts to become eligible for settlement.

- While accounts remain unpaid, interest and penalty fees may continue to accrue, increasing the total amount owed.

- Forgiven debt is generally considered taxable income under federal law.

- Even with negotiated reductions, the average client ends up paying more than 78% of their original balance.

Debt Settlement Offers No Guaranteed Results

Debt settlement companies cannot guarantee creditors will agree to settle your debt. Programs may take years to complete, and some consumers leave before resolving their balances.

Important Facts

- Creditors are not required to negotiate

- Settlement offers can be denied

- Results vary widely by creditor and account status

- Some consumers experience continued collections activity

Talk to a GreenPath Counselor

Before enrolling in a debt settlement program, talk with a certified financial counselor who can help you reduce debt and regain control without unnecessary fees or long-term damage to your financial health.

Legal Risks of Debt Settlement and Consumer Complaints

When accounts go unpaid, creditors may escalate collection efforts. In some cases, debtors may face lawsuits, judgments, wage garnishment, or additional fees.

The Better Business Bureau reports complaints about some debt settlement companies involving:

- Misleading claims

- High fees

- Poor customer service

Bottom line: This path can expose you to significant consequences—and some providers don’t always deliver on what they promise.

GreenPath’s Debt Management Program Structures Debt Repayment That Puts You First

If you’re looking for a clear, structured path to payoff, a Debt Management Program (DMP) may be worth exploring. A DMP typically consolidates eligible debts into one monthly payment, and payments are distributed to creditors on your behalf.

GreenPath Can Help You Pay Off Debt

A Debt Management Program (DMP) simplifies debt repayment by combining eligible debts into one monthly payment. Unlike debt settlement, a DMP provides a structured, lower-risk path to paying off debt over time.

Benefits of a Debt Management Program

- Lower interest rates

Average reduced to 6.6%, compared to approximately 28% prior to enrollment - Reduce monthly payments

Clients lower payments by an average of $199 per month - Pay off debt faster

Repayment occurs an average of seven years sooner

Calculate Your Savings

Use GreenPath’s debt management calculator to see how much you can save on the Debt Management Program.

Take the First Step, It’s Free and Confidential

Contact GreenPath to conduct a free debt counseling session to see if our debt management plan is right for you.

NOTE: this is an example. It helps you see how a debt management program might help you. IT IS NOT AN ACTUAL QUOTE.

How Your Debt is Calculated

The pay “on your own” example assumes you make only the minimum payment.

We use an interest rate of 24%, the GreenPath Debt Management Plan example shown is based on getting rid of your debt within 5 years.

We use an average interest rate of 8%.

In most cases, we can work with your creditors to reduce your interest rate. Actual interest rates will vary by client and creditor.

*Average results are based on GreenPath clients enrolled in a Debt Management Program; results vary by creditor, balances, and budget.

Trusted Nonprofit Guidance

Since 1961, GreenPath has helped people navigate financial challenges with clarity and confidence. As a national nonprofit, we put education first—so you can make informed decisions.

NFCC and HUD certified counselors, trained to national standards

Personalized, one-on-one guidance based on your goals and full financial picture

Confidential, judgment-free support you can trust

No cost initial counseling session to explore your options

Free Financial Resources

Debt Solutions Decoded: Why Debt Management Beats Debt Settlement

Don’t fall for risky debt settlement traps. Discover why Debt Management is the safer, smarter way to rebuild your financial freedom.

Articles & Recorded Webinar

- The Difference Between Debt Settlement and Debt ManagementThe Difference Between Debt Settlement and Debt Management

Learn about the differences between debt settlement and debt management—including risks, costs, and credit score impact—so you can choose a safer path to get out of debt. - A Comprehensive Guide to Debt Management ProgramsA Comprehensive Guide to Debt Management Programs

Learn how a Debt Management Program (DMP) works, what it costs, and how nonprofit credit counseling can help you pay off debt faster than going it alone. - Demystifying Financial CounselingDemystifying Financial Counseling

Learn what financial counseling is, what to expect, and how certified counselors can help you manage debt, build a budget, and support your overall financial health.