When considering debt consolidation, it’s crucial to weigh the costs and potential pitfalls.

While debt consolidation can improve credit scores through better payment management, it also carries risks of accumulating new debt if spending habits aren’t adjusted.

Consider debt management programsdebt management programs for a structured approach that includes financial education, potentially offering a more sustainable solution than consolidation.

The good news: you’ve decided to tackle your debt! The bad news: you don’t know what to do next. Which repayment strategy is best, and what’s the fine print?

First and foremost, you are not alone—with inflation and high-interest credit card rates, most Americans are feeling the burden, too. But before you leap into action, it’s important to understand the differences between two options you might be weighing: debt consolidation and debt management programs. Let’s look at both.

What is Debt Consolidation?

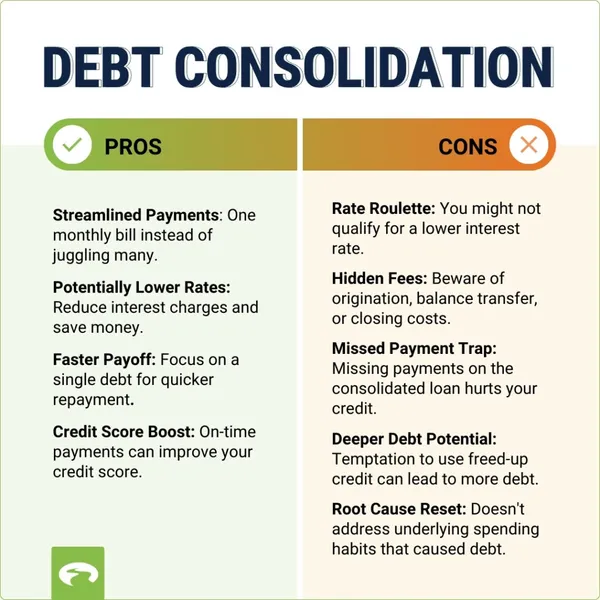

Debt consolidation involves rolling multiple debts into a single payment, usually with a lower interest rate. This can make managing your payments easier and potentially save you money on interest. While debt consolidation can offer temporary relief from high-interest rates and multiple bill juggling, you could fall into traps that worsen your financial situation if you don’t ask the right questions (we’ll get to that!)

How Does Debt Consolidation Affect Your Credit?

When you apply for a debt consolidation loan, lenders typically perform a hard inquiry on your credit report. This can cause a slight, temporary dip in your credit score. Once you consolidate your debts into one monthly payment, managing your payments becomes easier, reducing the likelihood of missed payments and benefiting your credit score.

On the flip side, if you don’t handle your consolidated debt responsibly, it can have adverse effects on your credit. Any missed or late payments on your consolidated loan can significantly damage your credit score and continuing to use your credit cards after consolidating could also lead to the accrual of more debt than you had originally.

Transform your finances with GreenPath’s expert support. Take charge of your money starting now.

800-550-1961877-337-3399What Are the Disadvantages of Debt Consolidation?

Fees and Costs

Debt consolidation loans can come with fees, including origination fees, balance transfer fees, and closing costs if you’re using a home equity loan. These fees can quickly add up and eat into any savings you might achieve through a lower interest rate. It’s crucial to factor these costs into your decision-making process.

Risk of Accumulating More Debt

One of the biggest risks with debt consolidation? The temptation to accumulate more debt. After consolidating, you might feel the freedom of financial breathing room and celebrate with more spending. This is especially risky if you consolidate credit card debt and then start using those cards again, potentially ending up in a worse financial situation than before.

Is Debt Consolidation a Good Way to Get Out of Debt?

Debt consolidation can be useful for some, but it’s not a one-size-fits-all solution. For it to be effective, you need to address the underlying habits that led to debt in the first place. Simply put, consolidation can be a quick fix rather than a long-term solution.

How Long Does It Take to Improve My Credit Score After Debt Consolidation?

The timeline for improving your credit score after debt consolidation varies based on several factors, including how well you manage your consolidated debt and your overall financial health. Typically, you may start to see improvements within a few months if you consistently make on-time payments and avoid taking on additional debt.

Can You Pay Off Debt Consolidation Early?

Most debt consolidation loans allow for early repayment without penalties. Paying off your consolidated debt early can save you money on interest and help you become debt-free faster. However, it’s important to check with your lender to understand the terms and conditions before making extra payments.

Questions to Ask Lenders

Before opting for debt consolidation, there are several factors to consider—have these questions ready when talking with prospective lenders so you walk away feeling financially informed.

- What is the interest rate on the consolidation loan?

- Are there any fees associated with the loan?

- What is the repayment term?

- How will this loan affect my credit score?

- Are there any penalties for early repayment?

Debt Consolidation vs. Debt Management Program

Whereas debt consolidation involves combining multiple debts into a single loan with one monthly payment, often at a lower interest rate, debt management programs (DMPs) offer a holistic approach to tackling debt.

A DMP, facilitated by a reputable credit counseling agency, helps you create a structured plan to pay off your debts, typically within three to five years. The agency works with creditors to arrange lower interest rates and waive fees, making your monthly payments more manageable without the need for a new loan. This approach also includes financial educationfinancial education and budgeting support, empowering you to develop healthier financial habits.

Opting for debt management over debt consolidation can provide a more sustainable solution to your financial challenges. With a DMP, you receive ongoing guidance and support, helping you address the root causes of debt and staying on track to avoid future debt issues.

Next Steps

Wondering if debt consolidation is right for you? Schedule a debt consolidation counseling session to receive 1:1 advice from a certified counselor. At GreenPath Financial Wellness, we are ready to meet you exactly where you’re at and help you strategize a repayment plan that works for your situation.

GreenPath Financial Service

Free Debt Counseling

Take control of your finances, get tailored guidance and a hassle-free budgeting experience. GreenPath offers personalized advice on how to manage your money.