Financial independence is less about reaching a specific income level and more about creating financial stability, flexibility, and confidence in your daily life.

Small, consistent actions—like budgeting, saving for emergencies, and reducing debt—can help you build greater financial freedom over time.

If debt or financial stress is making it difficult to move forward, GreenPath can help you understand your options and create a personalized plancreate a personalized plan.

Financial independence is often portrayed as a distant milestone: retiring early, accumulating significant wealth, or never having to worry about money again.

But for many people, financial independence looks much different.

It might mean having enough savingshaving enough savings to handle an unexpected car repair. It might mean paying bills on time without relying on credit cards. It could mean feeling confident about your financial future instead of constantly worrying about what might happen next.

In today’s economy, financial independence is less about achieving perfection and more about building stability, resilience, and choice.

And if that feels challenging right now, you’re not alone. According to the Federal Reserve’s 2025 Economic Well-Being of U.S. Households report, 63% of adults said they could cover a $400 emergency expense using cash, savings, or a credit card paid off at the next statement, meaning more than one-third could not cover that expense in the same way.

The reality is that many households are balancing competing priorities, rising costs, and financial uncertainty. That’s why financial independence today isn’t about comparing yourself to someone else’s success story. It’s about creating more control over your own financial life.

What Is Financial Independence?

Financial independence means having enough financial stability and flexibility to make decisions that support your needs, goals, and well-being.

For some people, that means becoming debt-free. For others, it means building an emergency fund, improving their credit score, saving for retirement, or simply feeling less stressed about money each month.

Rather than focusing on a single financial benchmark, it may be more helpful to think about financial independence as the ability to:

- Meet your current financial obligationscurrent financial obligations.

- Handle unexpected expenses with greater confidence.

- Make progress toward future goals.

- Make financial decisions without constant fear or crisis.

Financial independence isn’t one-size-fits-all. Your version of financial freedom should reflect your unique circumstances, responsibilities, and priorities.

Signs You’re Building Financial Independence

Financial independence isn’t always marked by a major milestone. Often, it develops through small, consistent improvements over time.

You may be building financial independence if you:

- Understand where your money is going each month.

- Have started building emergency savings.

- Are making consistent progress on debt repayment.

- Have a plan for upcoming bills and expenses.

- Save regularly, even in small amounts.

- Monitor your creditMonitor your credit and financial accounts.

- Feel more confident making financial decisions.

- Seek support when you need guidance.

These actions may seem simple, but they create the foundation for long-term financial wellness.

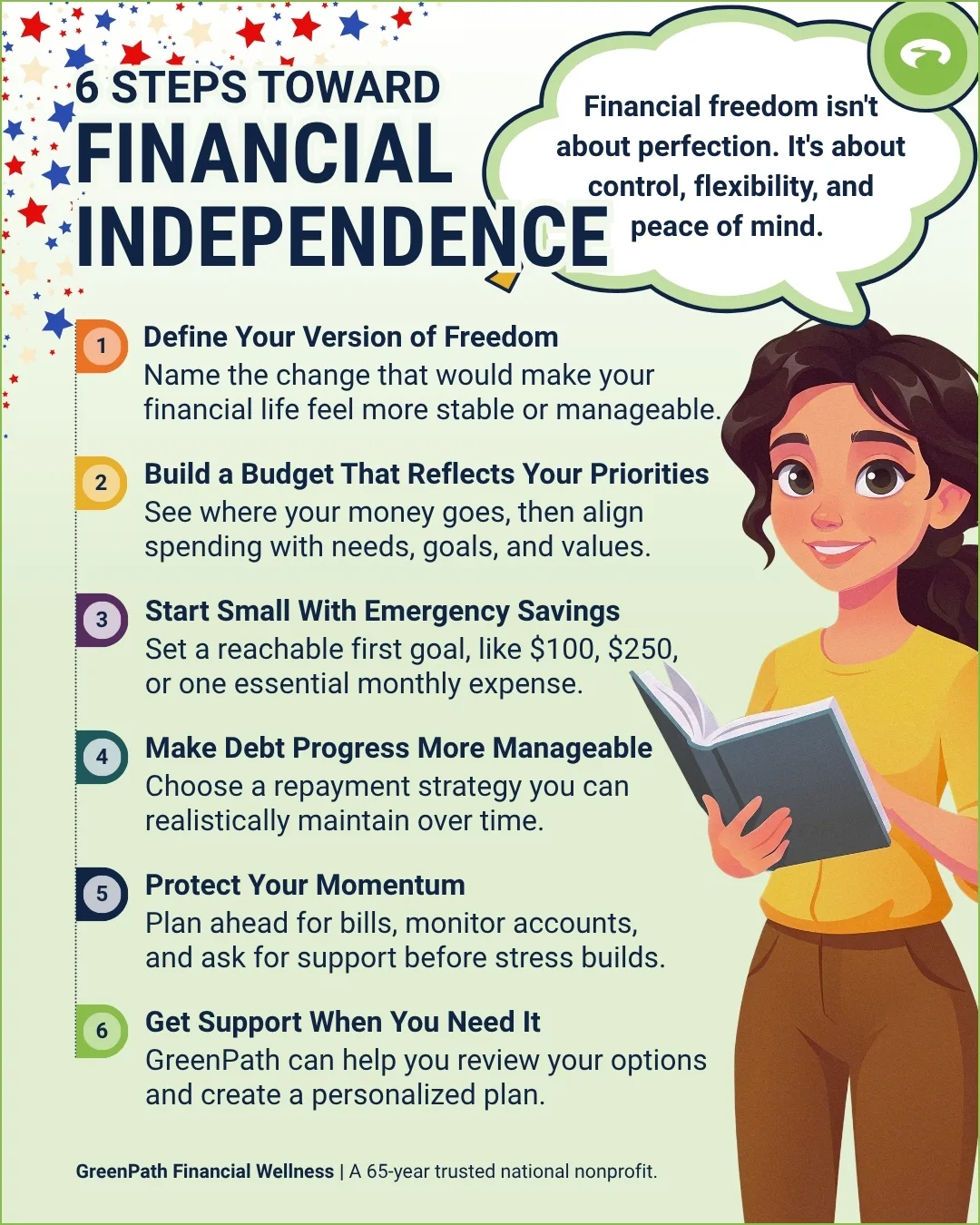

Step 1: Define What Financial Independence Means to You

Before setting financial goals, take some time to identify what financial freedom would look like in your life.

Start by reflecting on a few questions that connect your finances to your real life:

- What money challenge is causing the most stress right now?

- What financial change would make the biggest difference in your daily life?

- What do you want your finances to look like one year from now?

Your answer doesn’t have to be ambitious or dramatic.

Maybe you want to stop relying on credit cards for everyday expenses. Maybe you’d like to build an emergency fund or improve your credit score. Perhaps you simply want a budget that feels manageable.

Many people find financial goals easier to sustain when those goals are connected to their own priorities, values, and day-to-day needs.

Step 2: Create a Budget for Financial Independence

A realistic budgetA realistic budget is one of the most powerful tools for building financial independence.

Budgeting isn’t about restricting every dollar you spend. It’s about understanding where your money goes and making intentional decisions about how you use it.

Start by reviewing recent spending and organizing expenses into three categories:

- Needs: Essential expenses like housing, utilities, transportation, groceries, insurance, childcare, healthcare, and minimum debt payments.

- Wants: Discretionary expenses, such as entertainment, dining out, streaming services, hobbies, and non-essential shopping.

- Goals: Emergency savings, debt reduction, retirement contributions, education savings, and other future financial priorities.

If you’re struggling to make everything fit within your budget, don’t assume you’ve failed. Instead, use the information to identify where adjustments may be needed and what challenges require attention.

Step 3: Build a Starter Emergency Fund

Many financial experts recommend building enough savings to cover three to six months of essential expenses, though that goal can feel overwhelming when money is tight. Organizations such as the Consumer Financial Protection Bureau encourage households to build emergency savings gradually.

Instead of focusing on a large number, consider starting with a smaller, more reachable goal, such as $100, $250, $500, one utility bill, one week’s worth of groceries, or one insurance deductible.

An emergency fund helps create a buffer between unexpected expenses and additional debt.

Even a modest savings cushion can help cover common surprises like car repairs, medical expenses, household repairs, or temporary income interruptions.

If saving feels difficult, start small. Automatic transfers of just a few dollars per paycheck can help build consistency and momentum over time.

Step 4: Use a Debt Payoff Strategy to Reach Financial Independence

Debt can make it harder to achieve financial goals, especially when high interest charges consume money that could otherwise go toward savings or future plans.

Start by gathering key details for each debt, including the balance, interest rate, minimum payment, due date, and current account status.

Then consider a repayment strategy.

- Debt Snowball Method. Focus extra payments on your smallest balance first while making minimum payments on other debts. This approach can provide quick wins and motivation.

- Debt Avalanche Method. Focus extra payments on the debt with the highest interest rate first. This strategy can reduce total interest costs over time.

Seeking Additional Support

If debt payments feel unmanageable or progress seems impossible despite your best efforts, a nonprofit credit counseling agency like GreenPath can help you review your options.

Depending on your situation, support may include budgeting assistance, debt repayment strategies, creditor communication, or other solutions that help you work toward your financial goals.

The most effective debt strategy is typically the one you can realistically maintain over time.

Step 5: Protect Your Progress

Building financial independence isn’t only about saving more or paying off debt. It’s also about protecting the progress you’ve already made.

Helpful habits include reviewing account balances regularly, tracking upcoming bills and due dates, monitoring subscriptions and recurring charges, checking your credit reports periodically, planning ahead for predictable annual expenses, and communicating with creditors early if financial hardship arises.

Small preventive steps can help reduce financial setbacks and make future challenges easier to manage.

It’s also important to carefully evaluate any financial product or service that promises a quick fix. Before making major financial decisions, take time to understand the costs, risks, and potential consequences involved.

Step 6: Connect Financial Goals to Life Goals

Financial independence becomes more meaningful when it’s connected to something important in your life.

Your goals might include buying a homebuying a home, supporting your children, changing careers, starting a business, traveling, retiring comfortably, or simply feeling less stress about money.

Try framing your goals this way:

“I want to improve _____ so I can _____.”

For example: “I want to build emergency savings so I can handle unexpected expenses with confidence.” You might also focus on paying down credit card debt to free up money for future goals, improving your credit score to qualify for better financial opportunities, or understanding your budget so you can make more informed decisions.

This simple exercise can help transform financial independence from an abstract concept into a meaningful, achievable goal.

Financial Independence Starts with One Step (and Support When You Need It)

Financial independence doesn’t happen overnight, and it rarely follows a straight line. It is built through small, consistent decisions: tracking spending, saving when possible, paying down debt, planning ahead, and asking for help before financial stress becomes overwhelming.

A financial counselor may be especially helpful if you’re struggling to keep up with debt paymentsstruggling to keep up with debt payments, relying on credit cards for essentials, worried about missing upcoming payments, unsure which goals to prioritize, receiving collection calls, or needing help creating a workable budget.

Whether you’re just getting started or looking for a path forward, you don’t have to figure everything out alone.

GreenPath Financial Service

Debt Management Program

GreenPath is a 60-year trusted national nonprofit, learn how GreenPath’s Debt Management Program can help you pay off your debt in 3-5 years, while helping you develop sound financial literacy.